GTA Housing Market Report May 2026

Market Shows Gradual Signs of Improvement in April

Despite ongoing economic and geopolitical uncertainty, the GTA housing market showed signs of gradual improvement in April. Sales were up modestly from last year while remaining near historic lows, while new listings continued their downward trend this year, which helped to remove some inventory from the market. Average prices were at their lowest April level since 2020 but saw a slightly stronger-than-normal seasonal increase from March. Overall market conditions still favoured buyers, although some segments such as low-rise homes in Toronto have become more balanced.

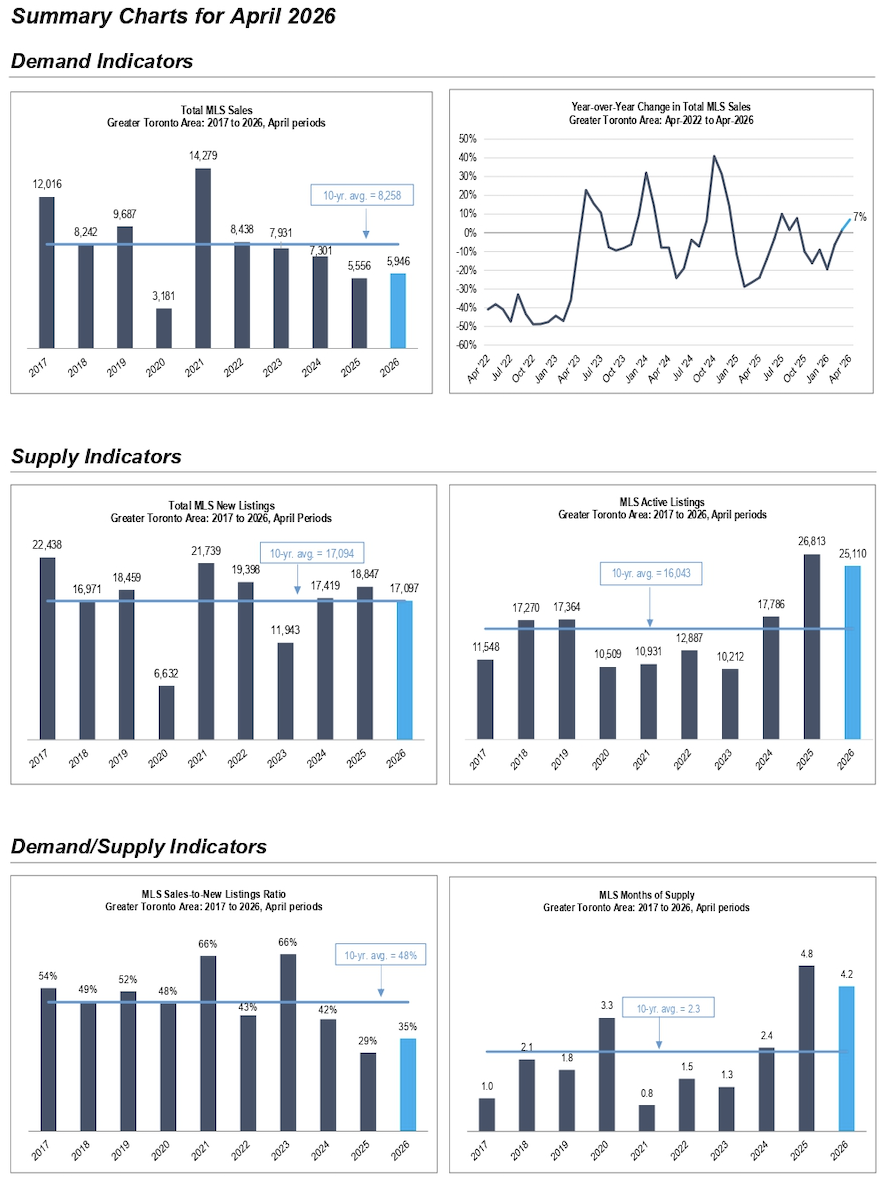

Sales Increase for Second Straight Month: The 5,946 MLS sales in April grew 7% from last year, increasing on an annual basis for the second straight month. However, outside of the initial COVID-19 period in 2020, this represented the second lowest April total for sales of the past 26 years. Sales in April were 28% below the 10-year average, with year-to-date sales down 3% from last year.

New Listings Fall Back to 10-Year Average: New listings fell for the fourth month in a row during April with a 9% year-over-year decline to 17,097 homes — directly in line with the 10-year average. The increase in sales and decrease in new listings brought total active listings at month-end down by 6% from last year to 25,110 homes, which was 57% higher than the 10-year average and the second highest April level for inventory since 2008.

Months of Supply Declines to 16-Month Low but Market Still Favours Buyers: The sales-to-new listings ratio improved to 35% from 29% a year ago, while still signalling a buyer’s market by remaining well below a balanced level of 45-60% and representing the second lowest April level in 30 years. The 4.2 months of supply represented the lowest inventory level in 16 months while remaining close to double the 10-year average of 2.3 months.

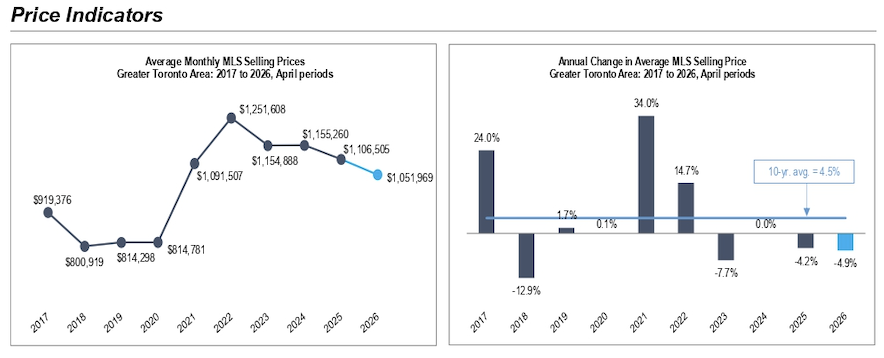

Selling Prices Show Signs of Stabilization: Average selling prices declined on an annual basis for the 15th straight month in April. However, the 4.9% decrease represented the smallest annual decline in seven months. Furthermore, the 3.4% month-over-month increase in average price was slightly larger than the typical seasonal uptick between March and April, indicating some stability for prices. At $1,051,969, average prices were down 16% from April 2022 but still 29% higher than the pre-COVID average in April 2019.

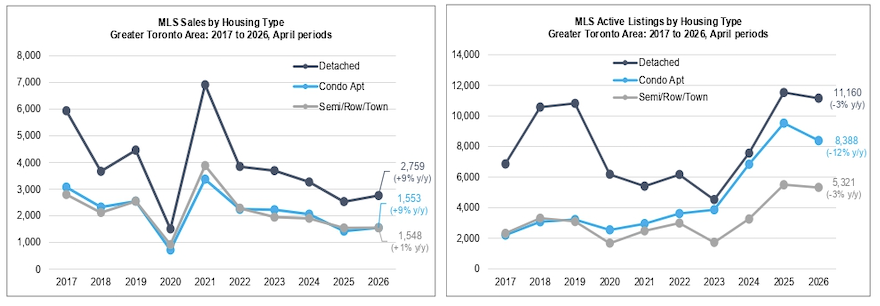

Detached and Condo Sales Up 9%: Sales for both detached homes and condo apartments rose 9% annually in April, while sales for semis/rows/towns were essentially flat with a 1% increase.

Double-Digit Drop in Condo Inventory: Active condo listings decreased 12% from last year to 8,338 units, which was still the second-highest April level on record and 81% higher than the 10-year average. Meanwhile, active listings for detached homes and semis/rows/towns both declined 3% annually. Compared to their 10-year averages, active listings were up 38% for detached homes and up 68% for semis/rows/towns.

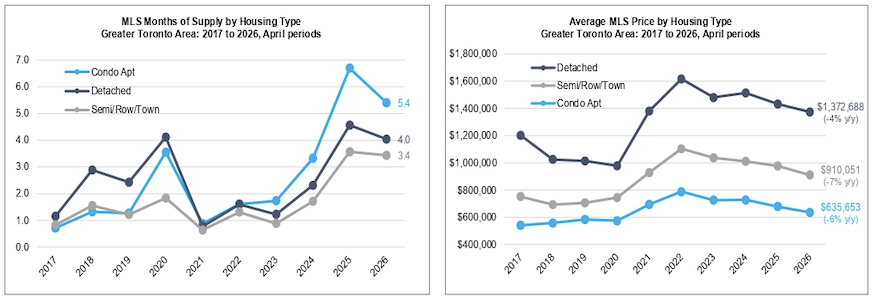

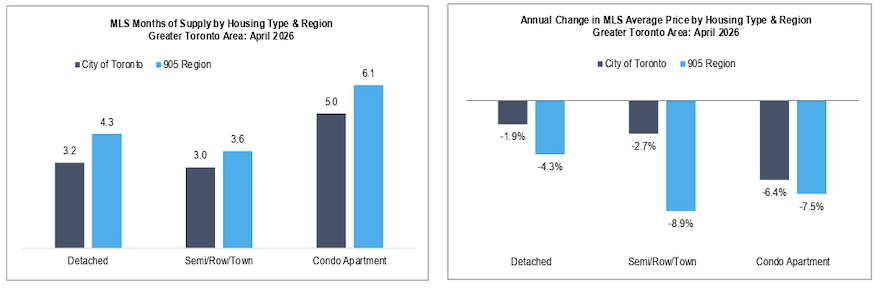

Months of Supply for Detached and Condos at 16-Month Low: Months of supply for condos was at a 16-month low of 5.4 months in April, dropping from 6.7 months last year but double the 10-year average of 2.7 months. Detached supply also fell to a 16-month low of 4.0 months, while supply for semis/rows/towns was essentially unchanged at 3.6 months.

Condo Prices Decline for 24th Straight Month: Condo prices declined on an annual basis for the 24th consecutive month with a 6.3% decrease to an average of $635,653 — down 19% from four years ago. Average prices for semis/rows/towns declined 6.8% annually to $910,051, while average detached prices held up best over the past year with a 4.1% decline to an average of $1,372,688. Over the past 10 years, condo prices have experienced the best appreciation, growing by a compound annual rate of 4.5%, compared to 4.4% for semis/rows/towns and 3.6% for detached homes.

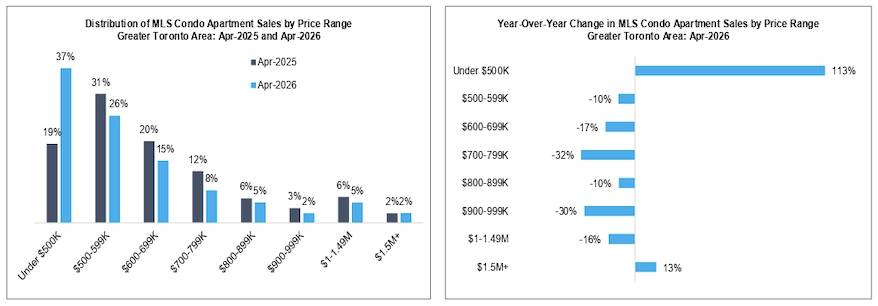

Nearly 40% of Condo Sales Under $500K: A 37% share of condos sold in April were under $500K, nearly double the 19% share from a year ago as sales rose 113%. This included a 9% share of units sold for under $400K (up from 2% last year) and a 28% share of units sold for $400-499K (up from 17% last year). The only other category of condo sales to see growth in the past year was high-end units priced at $1.5M+, which were up 13% in volume while representing a 2% market share.

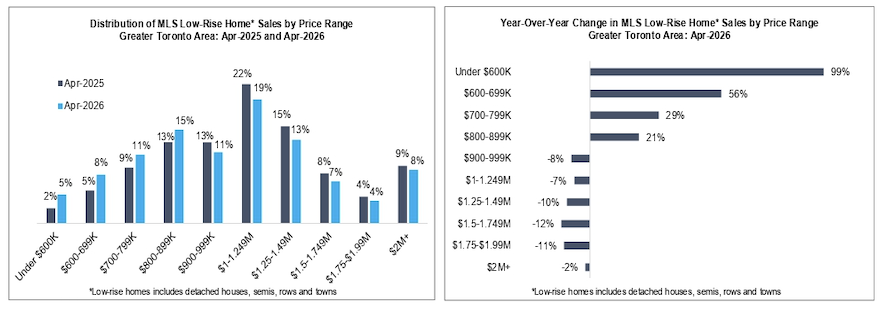

Low-Rise Sales Under $600K Double: For low-rise homes, sales increased over the past year for homes under $900K, including a 99% jump in homes selling for under $600K, representing a 5% market share. While low-rise home sales declined across all other price segments over $900K, activity held up best for the highest-priced homes selling for $2M+ with a 2% decrease, representing an 8% market share.

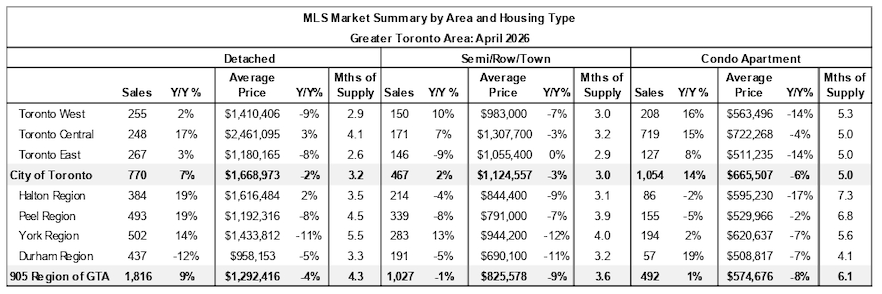

Detached Market Strongest in Highest-Priced Regions: Detached sales in the City of Toronto grew fastest within Central Toronto (+17%), pushing average prices up 3% annually to nearly $2.5M. The detached market in the 905 Region was strongest in Halton, where sales rose 19% and average prices grew 2% annually to $1.6M.

Central Toronto Condo Market Stabilizing: Condo sales in Central Toronto grew 15% annually in April while average prices decreased by a below-average amount of 4% to $722K. Condo supply was also below average in Central Toronto at 5.0 months.

City of Toronto Prices Holding Up Better than in 905: Across all housing types, average prices experienced smaller annual declines in the City of Toronto than in the 905 Region. The largest discrepancy was for semis/rows/towns, with average prices in Toronto decreasing 2.7% compared to an 8.9% annual decline in the 905.

Key Takeaways

A small amount of pent-up demand was released during April as buyers became more accustomed to the current economic and geopolitical uncertainty stemming from ongoing trade friction with the U.S. and the war in Iran.

For the third time this year, the Bank of Canada held its key interest rate unchanged at 2.25% in April even though inflation rose to 2.4% in March from 1.8% in February. So far, inflation was mostly contained to energy prices, with little evidence of pass-through to other goods and services. However, the Bank of Canada has said that if oil prices stay high and begin pushing up inflation more broadly, it might have to respond with rate increases.

Expectations of interest rate increases this year were diminished after the employment data was released for April, showing 18,000 jobs lost and unemployment rising to a six-month high of 6.9%. This helped to flatten bond yields and fixed-term mortgage rates, which should provide support for further growth in home sales in the months ahead. The weakening job market, however, will likely keep demand subdued.

With sellers becoming more hesitant to list in the current market environment, conditions are gradually becoming more balanced. This should help to limit further price declines, particularly in the low-rise segment in Toronto where supply is beginning to firm up.

While the condo market is still exhibiting oversupplied conditions, good progress back towards a balanced state has been made. New listings have been falling for eight straight months and active inventory dropped by its largest annual percentage amount in 50 months during April. This is occurring as prices have become more affordable, attracting strong demand in the entry-level segment, and completions are beginning to fall from record highs in 2024-2025.