Calgary Real Estate Market Update April 2026

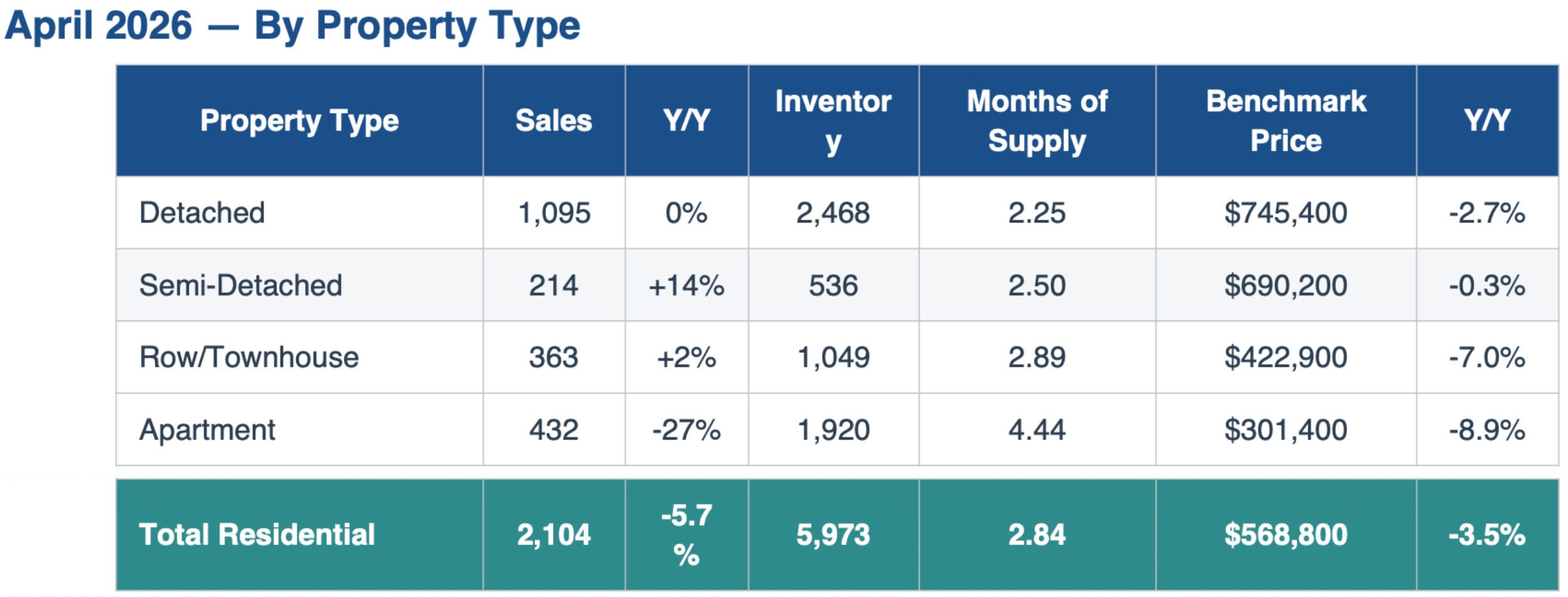

Calgary's housing market continued its gradual transition toward balance in April 2026. With 2,104 residential sales — down six per cent from April 2025 — and nearly 5,973 units sitting in inventory, the city is settling into conditions that haven't been seen since before the post-pandemic demand surge. The story, however, is one of two distinct markets: detached homes in key western and southern districts remain tightly held, while the apartment condominium segment has shifted firmly into buyer's market territory.

Price Snapshot

The unadjusted total residential benchmark price reached $568,800 in April — a modest seasonal uptick from March, though still 3.5 per cent below April 2025. The monthly gain was largely driven by the detached and semi-detached segments, which tend to lead price recovery heading into spring. The average sale price of $652,199 edged up 0.87 per cent year-over-year, reflecting the strength of the detached segment keeping the overall average elevated even as benchmark prices soften.

Apartment-style units tell a different story. The benchmark for that segment fell to $301,400, a year-over-year decline of nearly nine per cent — the steepest of any property type. With over four months of supply in the apartment market, there is little near-term upward pressure on condo prices. Buyers in this segment have more choice and more negotiating room than at any point in recent years.

Activity Snapshot

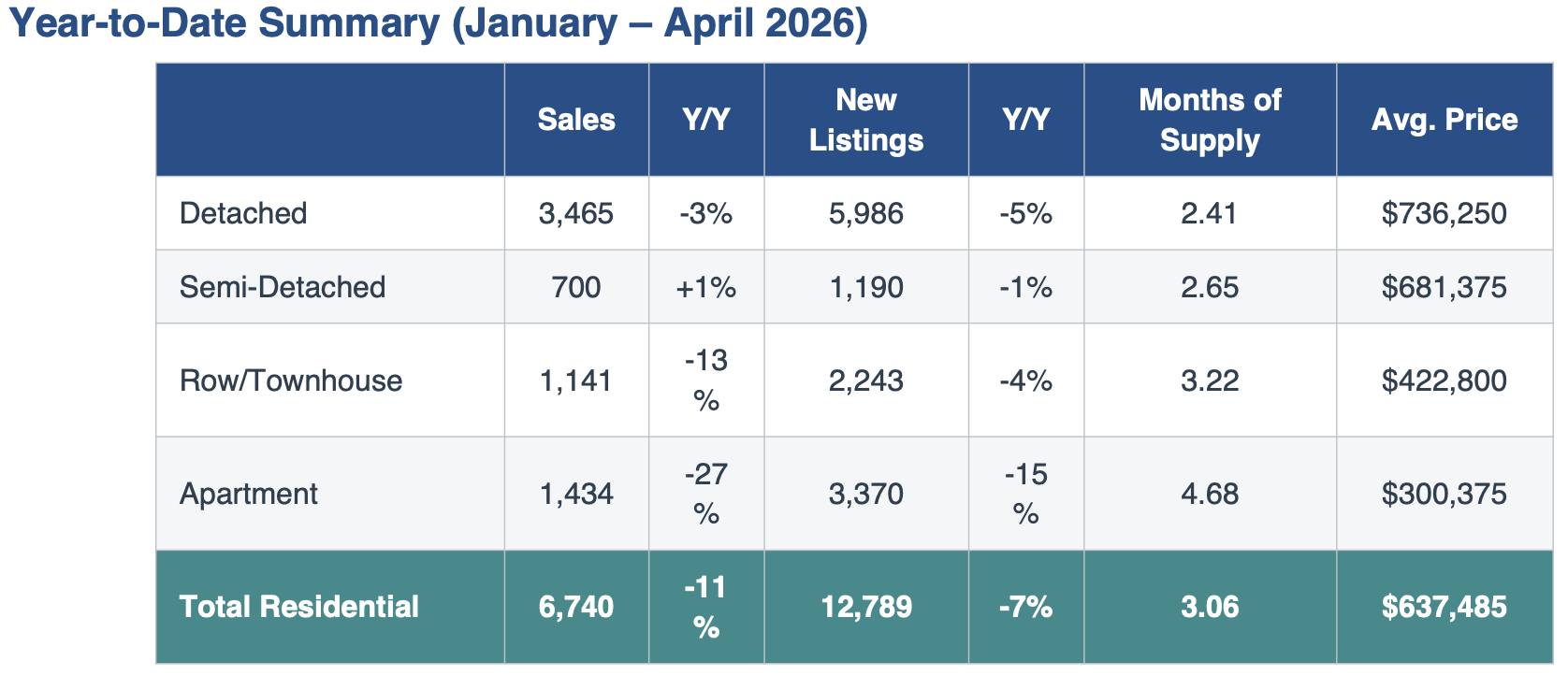

Sales activity in April picked up from March in line with typical seasonal patterns, but the year-over-year comparison tells the fuller story. Total sales of 2,104 units are six per cent below April 2025 and, year-to-date, sales sit 11 per cent behind the same period last year. Much of that gap is concentrated in the apartment segment, where sales fell 27 per cent year-over-year — a reflection of the pullback in demand as migration growth moderates and elevated condo supply gives buyers far more options than they had in 2024.

Homes are also taking longer to sell. Days on market averaged 35 days in April 2026, up from 29 days in April 2025 — a 21 per cent increase. Year-to-date, the average sits at 39 days, compared to 32 days over the same period in 2025. For sellers, this means pricing strategy matters more than it did in the past two years. Well-positioned homes still move; overpriced listings are sitting.

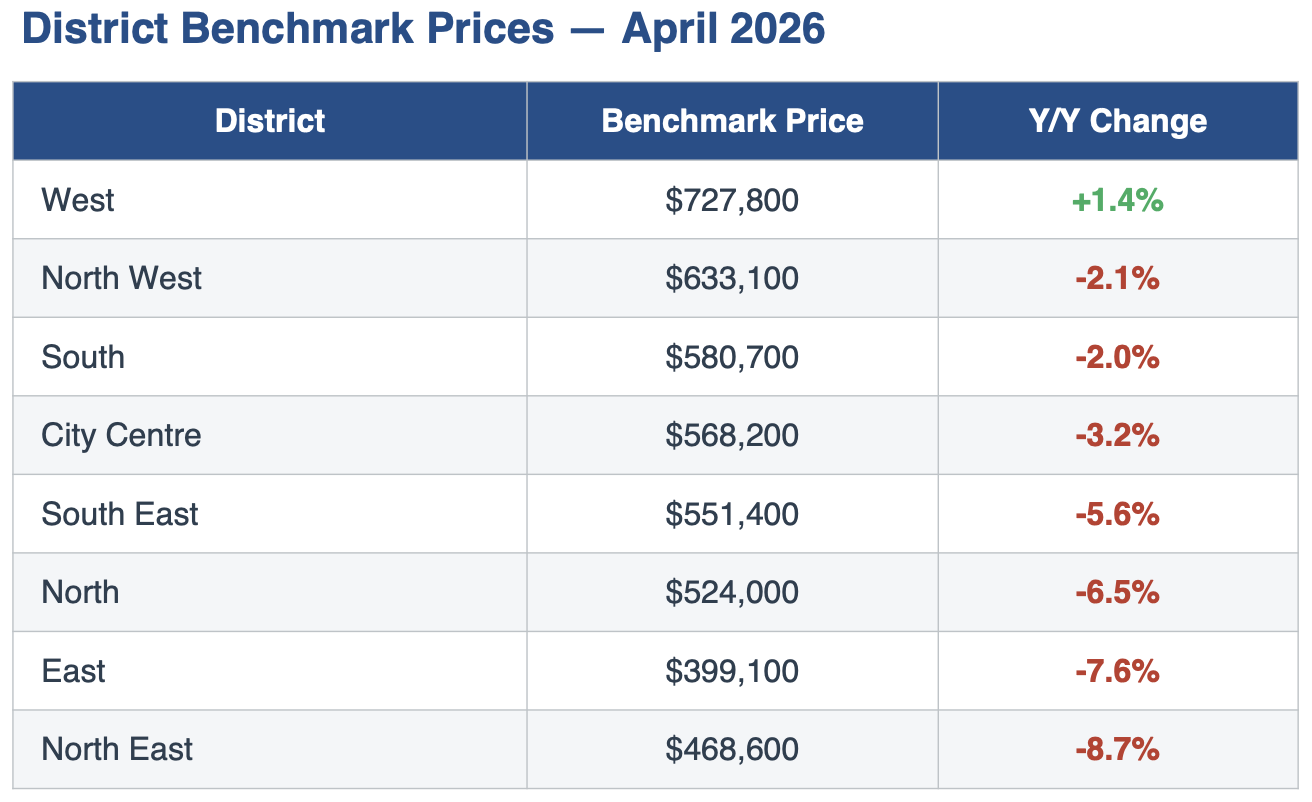

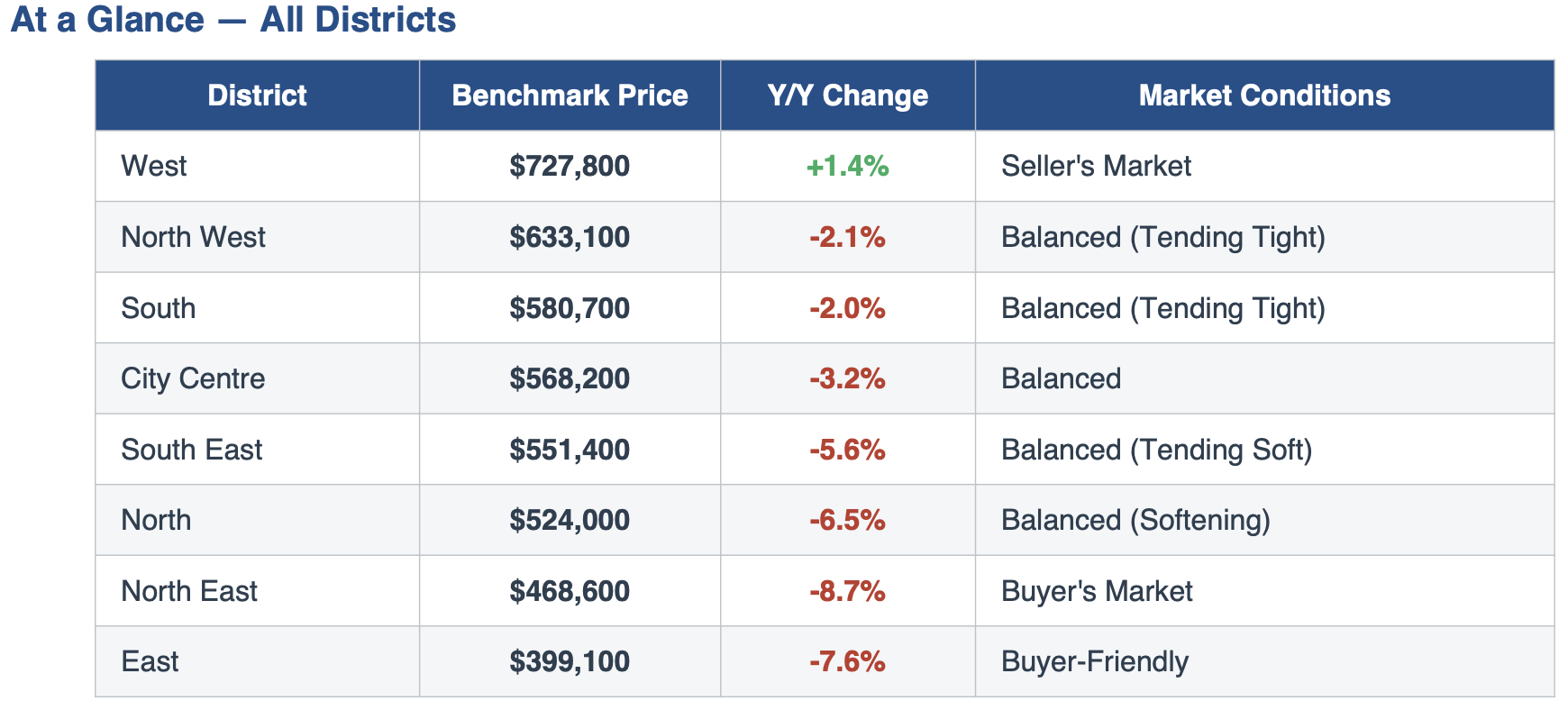

West Calgary is the only district posting year-over-year price gains (+1.4%), reflecting persistent tight supply in that corridor. North East Calgary has seen the steepest year-over-year decline at -8.7%, largely driven by condo and row inventory build-up.

What This Means for Buyers and Sellers

For buyers: The overall shift toward balance is welcome news, particularly in the apartment and row segments where supply is plentiful and sellers are more willing to negotiate. Detached buyers in high-demand pockets — especially West, North West, and South — should still expect competition and tight inventory. Getting pre-approved and acting decisively remains important in those areas.

For sellers: Accurate pricing is the most important decision you will make. With days on market up 21 per cent year-over-year and buyers having more options across most segments, homes that are priced to reflect current conditions are selling — and those that are not are sitting. The market has not turned against sellers in the detached segment, but the cushion for overpricing has narrowed considerably.

Every client's situation is unique, and the headline numbers only tell part of the story. Whether you are thinking about buying, selling, or simply keeping an eye on where things are headed, I am happy to walk through what these numbers mean for your specific price range and neighbourhood. Reach out anytime — I am here to help.

Calgary Market Update — April 2026 | District Summaries

The following summaries break down April 2026 market conditions across Calgary's eight geographic districts. Conditions vary considerably — from seller's market pockets in the West to buyer-friendly territory in the North East. Benchmark prices are unadjusted total residential figures sourced from CREB®.

BENCHMARK PRICE: $727,800 (▲ +1.4% Y/Y)

The West district is the standout performer in Calgary's April market — the only district recording year-over-year price gains at +1.4%. With less than two months of supply in the detached segment, conditions here remain firmly in seller's market territory, sustaining steady upward price pressure through the spring.

Buyers competing in the West should come prepared. Well-priced detached homes are still moving quickly, and multiple-offer situations remain possible in key pockets. The district's strong fundamentals — proximity to the mountains, established communities, and limited new supply — continue to underpin values.

BENCHMARK PRICE: $633,100 (▼ -2.1% Y/Y)

North West Calgary remains one of the more resilient districts in the city. The overall residential benchmark sits at $633,100 — down just 2.1 per cent year-over-year — with the detached segment benefiting from seller's market conditions and less than two months of supply. Prices in this segment have been rising month-over-month, easing the pace of annual declines.

Semi-detached and apartment prices in North West have also shown relative stability, with the semi-detached segment recording year-over-year improvements. For buyers, this district offers a balance of established amenities, transit access, and relatively contained inventory — competition is present, particularly for detached homes in the mid-range.

BENCHMARK PRICE: $580,700 (▼ -2.0% Y/Y)

The South district is holding up well in a softening market, posting a modest 2.0 per cent year-over-year benchmark decline. Detached homes continue to experience seller's market conditions — consistent with the North West and West districts — with limited inventory keeping dollar price pressure at bay in that segment.

The South's mix of newer suburban communities, family-oriented infrastructure, and relatively affordable detached options (compared to the West) continues to attract steady demand. Sellers of well-maintained detached homes can reasonably expect strong interest if priced accurately; condo sellers should be mindful of the broader apartment market softness.

BENCHMARK PRICE: $568,200 (▼ -3.2% Y/Y)

City Centre's benchmark of $568,200 — down 3.2 per cent year-over-year — reflects the pull of a softening condo market against a more stable attached and semi-detached sector. Semi-detached prices in the City Centre have shown year-over-year improvements, a positive signal for that segment's resilience amid broader price adjustments.

With a high concentration of apartment-style product, City Centre feels the effects of the citywide condo supply build-up more acutely than lower-density districts. Buyers looking for inner-city condos are in a favourable position, with more listings and greater negotiating room. Detached and semi-detached buyers will find a more competitive but still reasonable market.

BENCHMARK PRICE: $551,400 (▼ -5.6% Y/Y)

South East Calgary is recording a more notable year-over-year benchmark decline at -5.6%, driven in part by weaker conditions in the apartment and row segments. Apartment prices in the South East have been among the more affected in the city, with inventory levels rising and buyers having clear leverage in that segment.

Detached homes are faring better — the broader city pattern of tighter detached conditions applies here, though the South East does not carry the same supply constraints as the West or North West. For sellers, pricing to current conditions is essential; for buyers, the district represents good value relative to comparable product in the South or City Centre.

BENCHMARK PRICE: $524,000 (▼ -6.5% Y/Y)

The North district has seen a more significant year-over-year price adjustment, with the benchmark declining 6.5 per cent to $524,000. Apartment prices in the North are continuing to trend downward, reflecting the citywide condo oversupply story. Activity levels remain in a balanced range, but the direction of price pressure is clearly downward.

For buyers, the North offers relative affordability within Calgary — particularly in the apartment and row segments — with access to established communities and transit corridors. Sellers should approach pricing conservatively, especially in the condo segment, and be prepared for longer days on market than were typical in 2024 and early 2025.

BENCHMARK PRICE: $399,100 (▼ -7.6% Y/Y)

East Calgary carries the second-steepest year-over-year benchmark decline in the city at -7.6%, bringing the district benchmark to $399,100 — the most affordable of any Calgary district. The semi-detached segment is showing higher months of supply, and apartment prices are continuing to move lower, reflecting buyer-side leverage across multiple property types.

The East remains an entry-level and investor market, and for buyers focused on affordability, current conditions offer real opportunity. Sellers, particularly those holding condo or semi-detached product, should be realistic about the current environment and price to where the market is — not where it was twelve months ago.

BENCHMARK PRICE: $468,600 (▼ -8.7% Y/Y)

North East Calgary has experienced the sharpest year-over-year price correction in the city, with the benchmark falling 8.7 per cent to $468,600. Conditions across property types have shifted firmly toward buyers: the detached segment here — unlike most other districts — is reporting buyer-side conditions, with prices trending down from the previous month. The row segment has the highest months of supply and the steepest year-to-date price adjustments in the city, at over 11 per cent.

Apartment prices in the North East have seen some of the largest declines citywide. For buyers, this district offers meaningful value relative to the rest of Calgary, and conditions favour careful negotiation. Sellers should be prepared for a more challenging environment and must price competitively to attract offers in reasonable time.